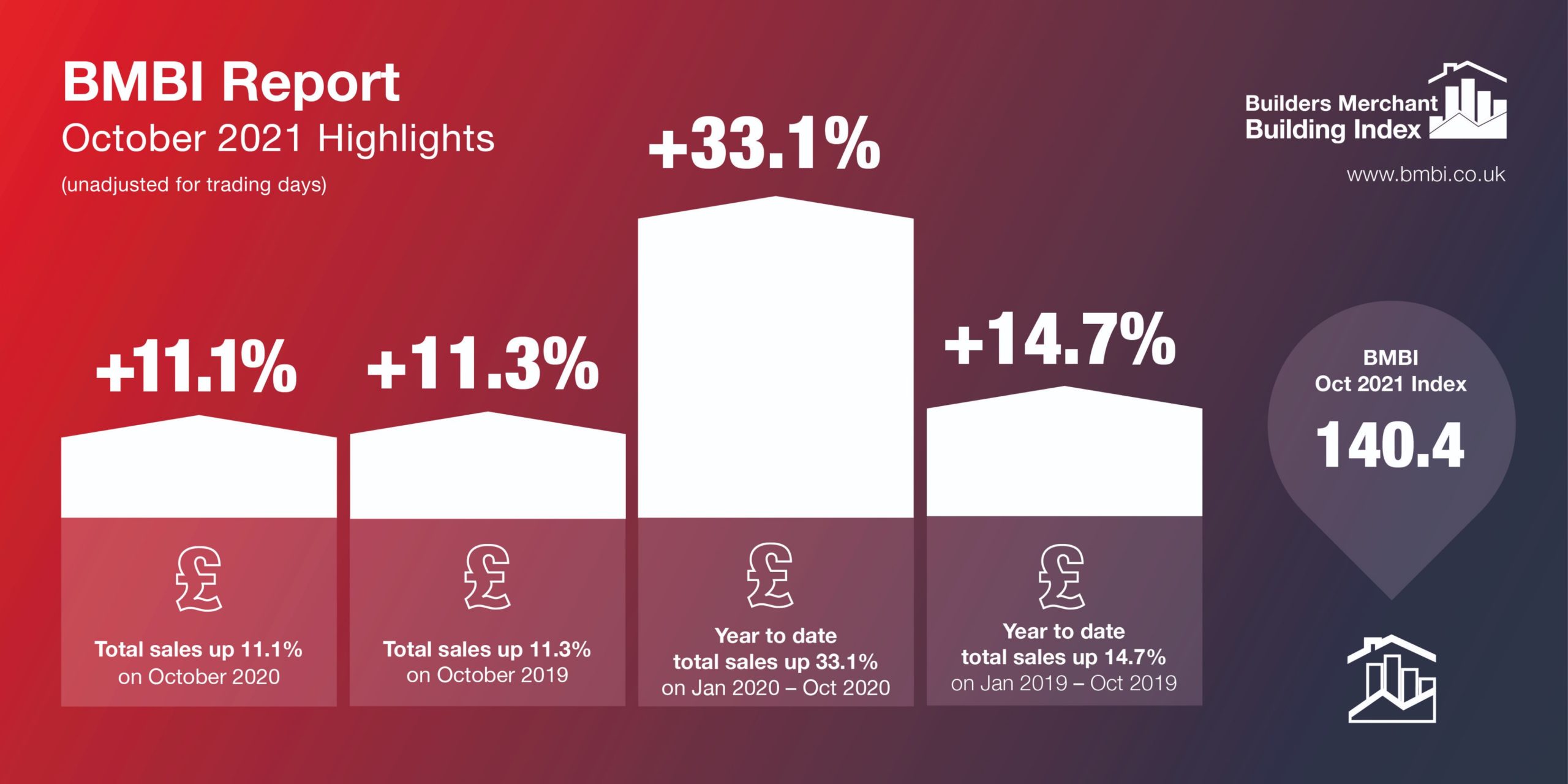

Demand for steel lintels has remained strong, but as a result of escalating material and labour costs, we saw the price shoot up at the beginning of Q3. This would normally result in high volumes sold, however, for the first time I know of in my career, we had to put steel lintels on allocation to help manage the restricted supply of raw material. Allocations were calculated based on the average purchased in the six months from 2019, and by branch.

Demand for steel lintels has remained strong, but as a result of escalating material and labour costs, we saw the price shoot up at the beginning of Q3. This would normally result in high volumes sold, however, for the first time I know of in my career, we had to put steel lintels on allocation to help manage the restricted supply of raw material. Allocations were calculated based on the average purchased in the six months from 2019, and by branch.

Despite these restrictions, we have so far been able to deliver 2.5% more tonnes of steel lintels in 2021 compared to 2019, so supplies are still getting through. It is fair to say that orders did not always arrive fully shipped and on time, however our teams behind the scenes have been working tirelessly to satisfy customer demands as best they can in the current conditions.

That said, we are part of a global supply chain and there are still serious challenges. The new barrier to normality is the pending energy crisis, with some factories in China reportedly working two days on and two days off to share the country’s energy resources. It is inevitable this will affect the global steel market, particularly in terms of availability and future pricing.

The NHBC is reporting completions in Q3 2021 compared to 2020 are down 5% (1692 units), reflecting the combination of last year’s post-lockdown recovery compared to the material challenges of 2021. On a more positive note, NHBC reports that 36% of new homes registered are detached, which is up from 28% on the same period last year, while apartments registered in Q3 2021 fell from 29% to 13%. With detached houses on the increase, coupled with new building regulations, demand for high thermal performing lintels is also set to rise.

The NHBC is reporting completions in Q3 2021 compared to 2020 are down 5% (1692 units), reflecting the combination of last year’s post-lockdown recovery compared to the material challenges of 2021. On a more positive note, NHBC reports that 36% of new homes registered are detached, which is up from 28% on the same period last year, while apartments registered in Q3 2021 fell from 29% to 13%. With detached houses on the increase, coupled with new building regulations, demand for high thermal performing lintels is also set to rise.

Looking ahead, we believe the industry will see a reduction in raw material shortages and supplies becoming more stable in Q4, which will in turn slowly improve overall service levels for steel lintel customers.

Recent Comments